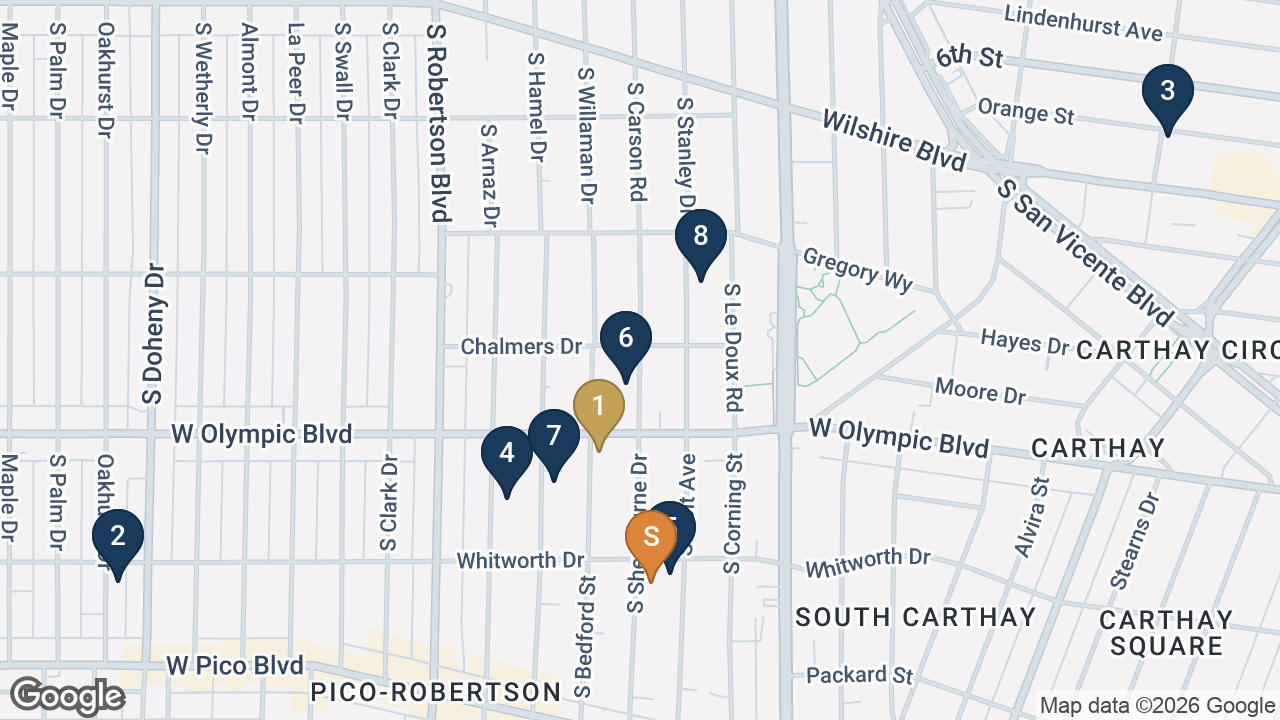

Comparable set drawn from the LAAA Team's own Marcus & Millichap sale of 1010 S Bedford St and its underwritten sold-comp file for the immediate submarket. Several comps sit within blocks of the subject — including 919 S Sherbourne Dr, on the same street.

1. 1010 S Bedford St — SOLD by the LAAA Team (just closed). Our own Marcus & Millichap closing and the single most relevant trade in the submarket: a 1963-built, elevator-served 12-unit Pico-Robertson building sold for $3,650,000 ($304,167/unit, $283/SF, 5.16% cap). The campaign generated over 15 property tours and 6 written offers across a disciplined four-month, ~10-buyer process (listed $3,900,000, reduced to $3,800,000 then $3,725,000), and closed all-cash in a seven-day escrow to meet a buyer's 1031 exchange deadline — direct, first-hand evidence of live demand and pricing in this exact pocket.

6. 919 S Sherbourne Dr — The most location-relevant comp: a 1958 5-unit on the subject's own street, sold Nov 2025 at $2,240,000 ($448,000/unit, $390/SF, 4.96% cap). Its tight cap and high per-unit basis on a smaller building underscore the strength of the immediate Sherbourne rental pocket.

2–3. 1110 S Oakhurst Dr & 650 S La Jolla Ave — The two larger 12–13 unit trades ($345,769 and $358,333/unit at 5.24% and 5.41% caps) frame the going-in yield band for institutional-scale RSO product in the pocket.

4, 5, 7, 8. Wooster, Holt & Shenandoah — The cluster of 5–6 unit 1953–65 walk-ups ($297,500–$420,000/unit; 5.02%–5.04% caps where reported) brackets the subject's size and vintage most closely and anchors the $/SF range ($343–$407).

Averages exclude the featured 1010 S Bedford sale and are computed on the seven sold comps (#2–8). Cap rates shown where reported by the closing file.